How to Position Small Business Wealth Advisory to Your Clients and Your Firm

Most advisors aren’t equipped because the relationship was never structured to go there. The financial advisory industry has spent decades optimizing around investments. That model leaves business owners underserved at precisely the moments that matter most.

The Small Business Wealth Advisor™ (SBWA™) certificate program gives advisors the knowledge, frameworks, and language to change that. It’s the only program that prepares advisors to deliver sophisticated, full-lifecycle financial planning for business owners — not just exit strategies. But earning the credential is only half the equation. The other half is knowing how to talk about it with the clients who need it and the firms that should be investing in it.

Why this positioning matters now

The scale of the opportunity is hard to overstate. There are 33 million small businesses in the United States, employing nearly half the American workforce.¹ Yet the financial planning industry has largely treated them as a secondary segment — too complicated to serve well, too fragmented to pursue systematically.

The cost of that inertia is measurable:

- Approximately 595,000 businesses close in the U.S. every year.² Each closure represents lost jobs, lost wealth, and, for the advisors involved, a client relationship that walks out the door.

- Only one in two small businesses survives past five years. Just one in three makes it to ten years.²

Advisors positioned to serve business owners at the planning level, not just the investment level, are entering a segment that is underserved, consequential, and increasingly willing to pay for genuine expertise.

How to position SBWA™ to clients

Business owners are not primarily thinking about their investment accounts. A business owner’s relationship with wealth is completely different. Their wealth is the business. It’s tied up in inventory, equipment, receivables, real estate, or the value of their client relationships.

That’s where the positioning starts. For a new client, the framing is direct: Your business is probably your most valuable asset. Does your financial advisor truly understand it?

For an existing client, the entry point is different. It’s not a challenge; it’s an opening. Something like:

I’ve helped you manage your investments and plan for retirement, but I want to make sure we’ve talked about your business. Not just as an asset on a balance sheet, but what it’s worth, where it’s headed, and what happens to it down the road. Have we ever really gone there?

From there, the conversation opens naturally. SBWA™-trained advisors are equipped to move beyond the investment account and address the questions that most advisors never ask:

- How is your business actually performing? What do the cash flows, income statements, and balance sheets reveal about where it’s headed?

- What does your personal financial future look like, independent of the business? If the business underperforms, or if you get sick, what’s the plan?

- What happens if something unexpected occurs? An illness, a partnership dispute, an unsolicited offer to buy — is there a plan in place?

- How does the business eventually transfer wealth? To a buyer, a family member, the next generation?

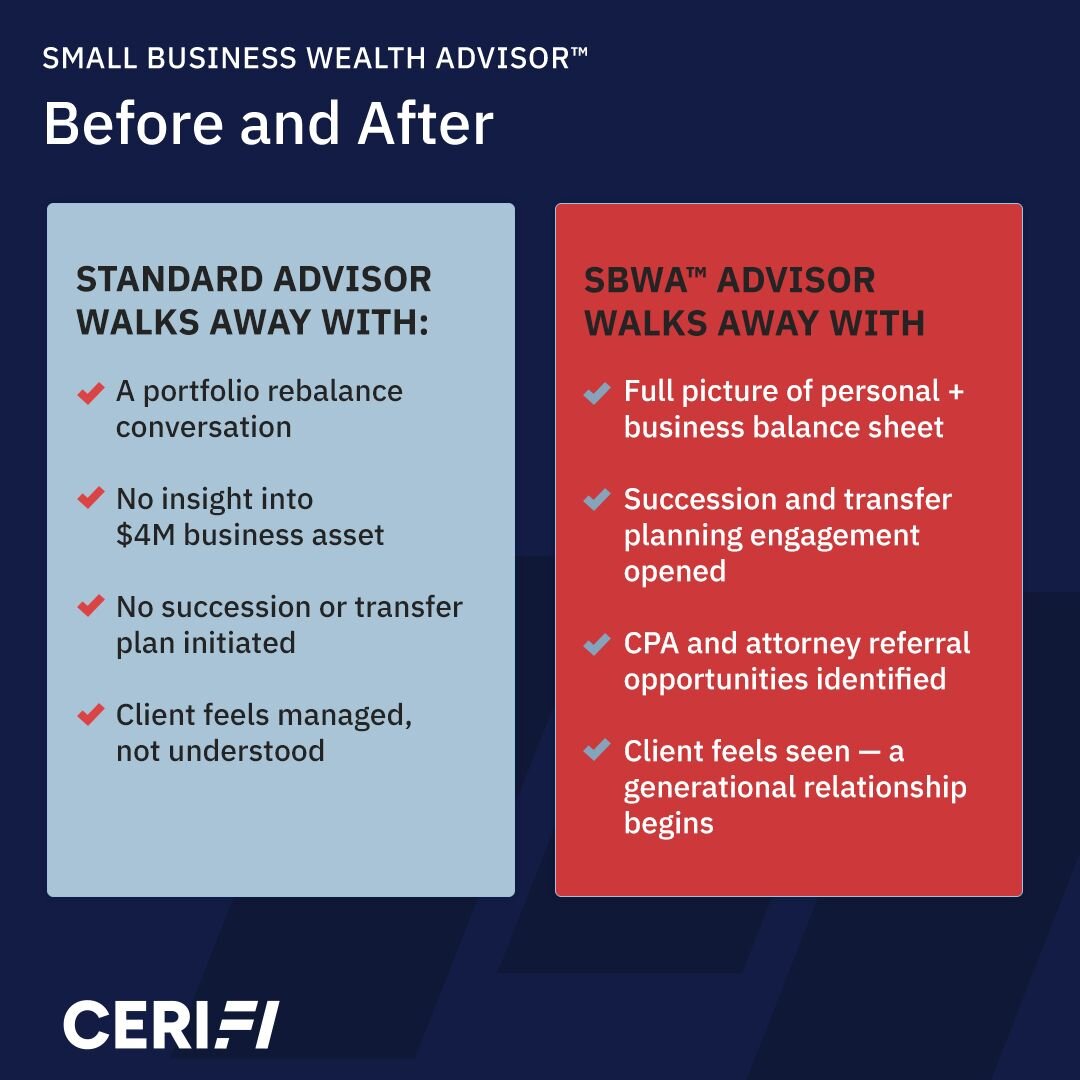

Most business owners have never been asked these questions by their financial advisor. The advisor who asks them and can help build the answers becomes something entirely different: a strategic partner, not just an investment manager. That’s the shift SBWA™ makes possible. Not a new service to sell, but a new kind of relationship to build.

SBWA™ gives advisors the vocabulary and frameworks to make that claim credibly — and to back it up immediately with the kind of questions that change the dynamic in the room.

Want to experience the SBWA™ program? Try a free module →

How to position SBWA™ to your firm

The conversation inside your firm requires a different frame: one that speaks to business outcomes.

Start with retention. Research shows that 70 to 80 percent of heirs leave their parents’ financial advisor when wealth transfers.³ Advisors who build deep, whole-life relationships with clients, including relationships that extend into the business, are the exception. They’re also the advisors that firms can’t afford to lose. SBWA™ is a direct investment in building those irreplaceable relationships.

Then make the AUM case. Clients whose businesses grow in value bring more assets under management. Clients who exit successfully — with advisor guidance — become long-term wealth management clients. Every business balance sheet conversation is an entry point for planning, insurance, and advisory services that a purely investment-focused relationship would never surface.

Finally, make the competitive case. Other firms are pursuing the small business segment. Advisors with a specialized credential in business-owner financial planning are more competitive, more productive, and more differentiated. No other credential addresses the full scope of small business financial planning — SBWA™ is purpose-built for it.

CFP® certification offers a useful analogy for the value expertise commands: CFP® professionals earn an average of 13 percent more than non-certified peers.⁴ Expertise commands premium value. SBWA™ represents a similar investment in depth, applied to a client segment most credentials have never touched.

The summary case for firm leadership is straightforward: SBWA™ doesn’t just upskill individual advisors. It equips your team to capture a client segment that competitors are actively pursuing. And it helps build relationships that survive market cycles and generational wealth transfers.

The language that works

Whether you’re talking to a client or firm leadership, two principles apply:

Lead with outcomes, not just credentials. Simply having a credential after your name isn’t enough to move people. What really moves people is the outcome on the other side: a business owner who exits successfully, an heir who stays with the firm, a client who says, I didn’t know my advisor could help me with that.

Avoid positioning SBWA™ as continuing education. It’s much more than that. It’s a strategic capability, a shift in what an advisor is able to do and the kind of relationship they’re able to build. The distinction matters, especially in a firm environment where training budgets are scrutinized and ROI is expected.

Both conversations, with clients and with firms, are ultimately expressions of the same message:

We’re on a mission to reduce the number of small businesses in America that fail. We believe that better-equipped advisors are the fastest path to better outcomes for business owners — and that when those outcomes improve, everyone wins: the owner, the advisor, the firm, and the economy itself.

That mission is the bridge. It resonates with a business owner who needs a better partner, and with a firm that needs a better story.

What SBWA™ actually equips you to do

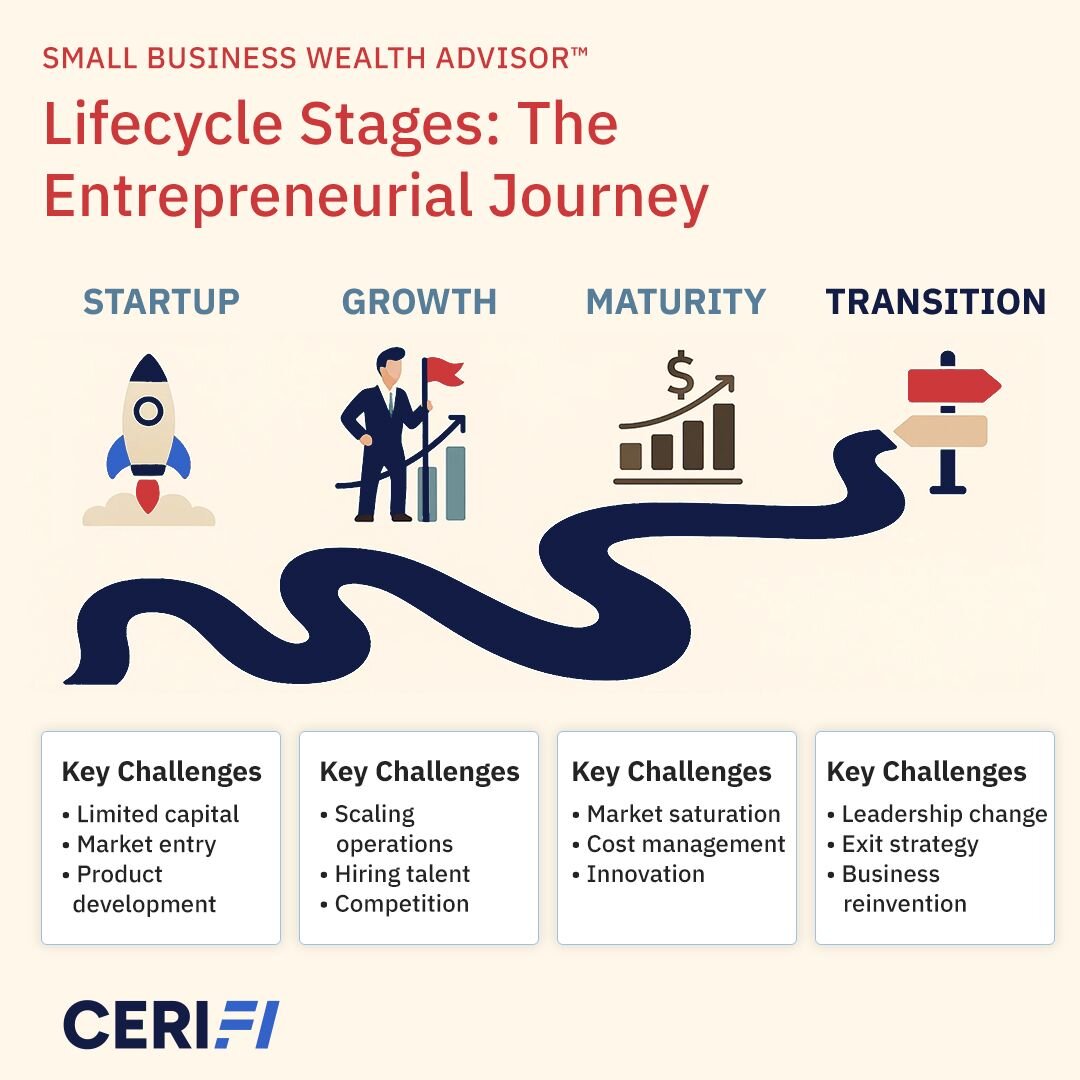

SBWA™ is a certificate program that leads to better outcomes for business owners at every stage of their journey, from the early days of building to the eventual moment of transition or exit.

The program equips advisors to analyze business performance, understand the personal financial picture that sits alongside the business, and plan for the full range of what-ifs: health events, partnership changes, succession decisions, and exits. These are conversations most advisors aren’t trained to have. After SBWA™, they are.

The advisor who guides a business owner through a successful exit earns something no prospectus can: trust that carries across generations. That’s the differentiator SBWA™ builds.

The advisors who step into the gap win

The demand is there. The gap is real. And the advisors willing to bridge it — by learning the language of business ownership and showing up as genuine strategic partners rather than investment managers — are the ones who build practices that last.

And the compounding benefit is clear: going upstream from exit planning doesn’t just deepen a relationship — it extends one. An advisor engaged only for an exit is in the picture for months, maybe a year or two at most. An advisor who walks alongside a business owner through the growth years, the succession questions, the what-ifs — that relationship runs 15 to 20 years or longer. The numbers tell the story.

The positioning, once understood, is not a hard sell. It’s the truth.

Learn more about the SBWA™ certificate program →

Sources

¹ U.S. Small Business Administration, Small Business Facts, 2024

² U.S. Bureau of Labor Statistics, Business Employment Dynamics, 2024

³ Cerulli Associates, as reported by CNBC, “Most heirs fire their parents’ wealth advisor. Here’s how advisors can keep them as clients,” October 16, 2025. cnbc.com/2025/10/16/heirs-parents-wealth-advisor-cerulli-study.html

⁴ CFP Board, 2025 CFP® Compensation Study. cfp.net/for-cfp-pros/financial-planner-compensation-trends

The Dalton Education Team

Talk to an advisor today.

Our advisors are your go-to for everything CFP®. Need course recommendations? Extend a course? We’ve got you covered.

Office hours: M-F, 8am-5pm EST